At Magenta we always ask about a client’s family situation and whether there is likely to be any financial support required for young children, older parents, adult children and/or other family members. It is important that we understand whether there will be any possible future demands on a client’s resources, so that the advice we provide is accurate and appropriate.

On the subject of financially supporting adult children, there are generally 2 opposing views:

- They’re on their own now! Many parents feel that once they have fed, housed and educated their children, perhaps to a certain determined age, they will then withdraw further financial support to encourage independence and a good work ethic.

- We will always be there for them! Others consider their children to be a lifelong project and expect whatever family money to always be available to help them whenever they need it.

In truth, our experience is that most parents will tread a middle path, helping their children where they can, but setting out expectations of what is possible and acceptable.

However, we have seen situations where adult children have almost bullied parents into giving them money that they can ill afford and will almost certainly adversely affect their standard of living in the future.

Similarly, sometimes adult children find themselves in difficult situations like divorce, or abuse or some sort of addiction, where parents feel compelled to help out financially, again often to their own detriment.

It is really important when discussing future financial planning to consider all the above possibilities and for a Financial Planner to be aware of any family relationships that may require financial assistance. Putting this kind of contingency planning into a lifetime financial forecast, will ensure that everyone can see the future picture clearly and work out whether gifts or loans to adult children are possible and if so to what extent.

Can you afford to give away money to adult children?

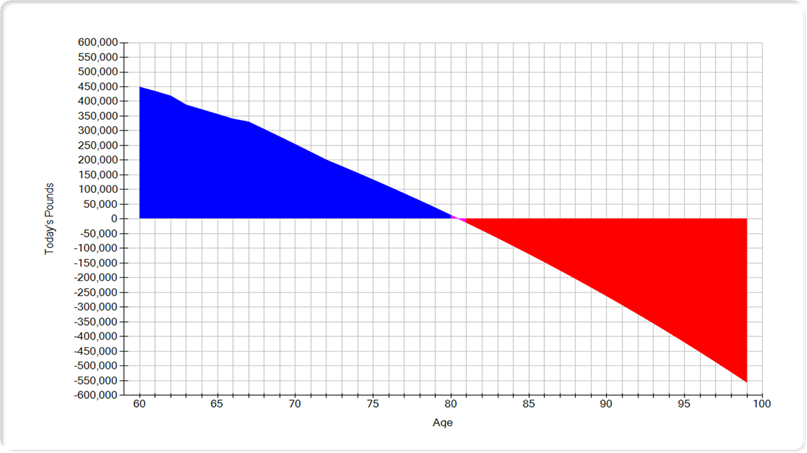

As a simple example, if Mr and Mrs Jones’ future cashflow looks like this, giving away money will make things worse and will definitely have an impact on their future security and happiness as they will run out of money sooner.

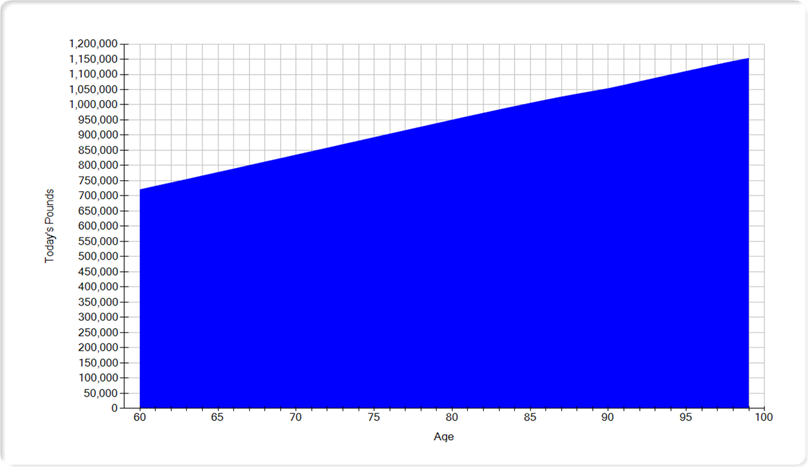

If however, it looks like this, there is clearly scope for making gifts or maybe helping with grandchildren’s school fees or paying for family holidays etc.

This is why it is so important to use cashflow forecasts to help people determine what they can and cannot afford to do in life.

But we have money to spare!

There is a common dilemma for parents with money to spare: When and how much should they give to an adult child who comes asking for money — especially one who is able-bodied and well-educated? How long should any financial help last? And should it be a gift, loan or advance on an inheritance?

As financial planners, we generally caution parents to carefully scrutinise the need for the money and how it could affect the child’s long-term ability to live, work and succeed in the world.

The biggest challenge is providing enough money to help a child through a challenge, but not giving to the point where it kills the person’s motivation and ambition.

Some needs, like education and re-training are compelling areas for giving money to children. This is often seen as an investment in a child’s long-term employment future.

But how should parents handle the growing number of young people, especially millennials, who are staying at home longer, marrying later — if at all — and relying on their parents for free rent, food, mobile phone and car insurance?

We would generally advise parents not to allow their adult children to live rent-free without any deadline and not to pay an allowance without any strings attached, otherwise there is a danger of creating an unhealthy dependency.

Tough Love

Having said that, there are other parents who take “tough love” to the extreme. They refuse ever to give an adult child money, even insisting that the child works to pay for college. Then, when they die, they leave their entire estate to an adult child who might no longer need it.

We recommend that parents give their children monetary gifts while they’re alive, (IF their cashflow forecast indicates they can afford to after securing their own future,) rather than leaving everything in a will. This helps adult children when they need it most, for buying a house etc and it can reduce inheritance taxes when a parent dies.

Should all children be treated the same?

Finally, a further consideration is whether to treat all children equally as far as financial gifts/loans are concerned, or take into account their individual circumstances.

Giving a child money for certain milestones, like college graduation, marriage or the birth of children may seem like a good idea on paper. But it can stoke feelings of anger and resentment in children who don’t marry or can’t have children.

We recommend that parents be open and fair when giving money to adult children. If money is given to one child, the other children should be informed and promised similar monetary gifts either now or at the time of inheritance. Intentions could also be written down and shared if appropriate within the family.

Most children keep a scorecard — even if parents don’t, and this can cause endless problems in the future, with deep rifts being created over money.

For example, we have a client who did not receive money in her parents’ will because she was wealthy in her own right. The estate was shared between her two brothers. She has been scarred by this experience and carries a great deal of hurt and anger, not because of the money so much, but what it represented – she now feels that her parents loved her brothers more than her. She no longer has a good relationship with her brothers, despite them understanding her feelings and wanting to even things up.

A complex theme

So as we can see, money and adult children is a complex theme, one riddled with deep emotions and sentiment.

Our advice is to keep talking to family about your thoughts and intentions – maybe write a letter of wishes to explain your actions if talking is not your forte.

If everyone understands parental motivations, financial matters, especially gifts, loans and inheritance will proceed more smoothly in the future.

If this subject is of interest or concern, do please call us for a friendly chat.