Help to Buy ISAs – Now or never?

We have received a few queries recently about whether or not clients should set up Help to Buy ISAs for their children, before they are withdrawn at the end of this month (30th November).

The short answer is, no! (or at least, probably not.)

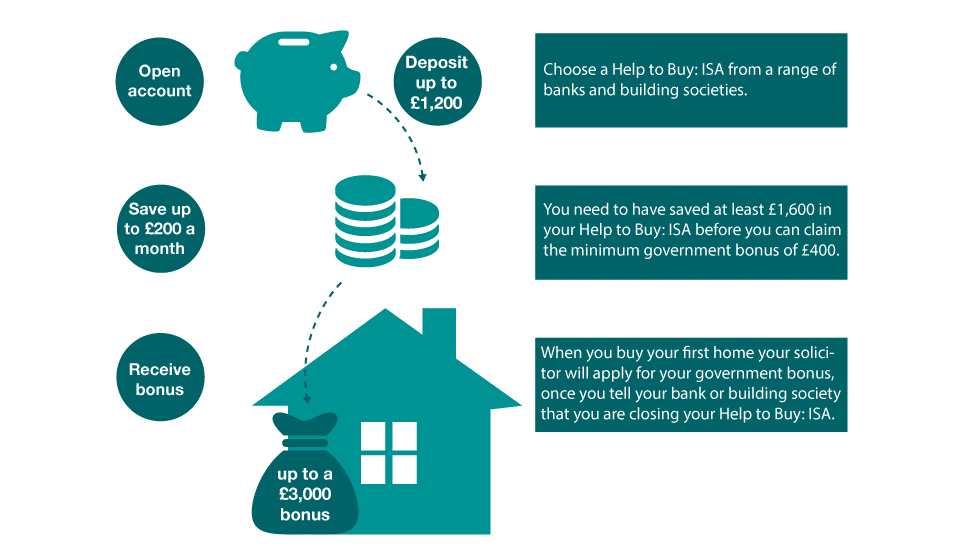

As a reminder, the Help to Buy ISA works as follows:

Whilst “free” money from the Government is always an appealing prospect, the appeal of the Help to Buy ISA has decreased significantly since the introduction of the Lifetime ISA (LISA) in 2017. The LISA also receives a Government bonus of 25%, but with slightly different limits and rules.

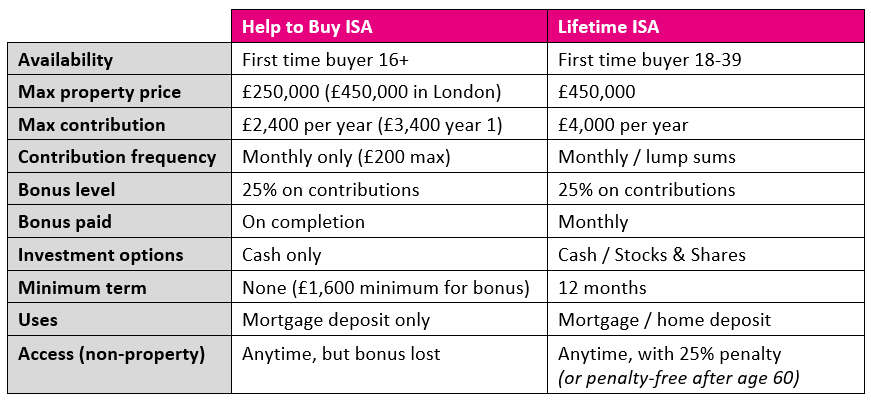

A comparison of the key features of these for a first home purchase are shown below:

In summary, the LISA has a higher savings limit (and therefore a higher available bonus), can be invested for potential growth over the long term (including compounded growth on the bonuses received), as well as a higher potential purchase price for non-Londoners.

Because of this, in the majority of cases, the LISA is probably going to be more suitable for savers.

That said, there are some important considerations which might mean that a Help to Buy ISA is still the best option:

- If you are planning to buy a home before you turn 19 a LISA won’t help you, given the minimum opening age of 18 plus the 12-month initial holding period.

- Similarly, if you’re over 18 but want to buy your home pronto, any LISA savings would not be able to be accessed for the first 12 months after opening the account.

- If you need to access the funds in an emergency, a 25% penalty will be applied to withdrawals from the LISA, equating to the bonus and a percentage of your initial contribution (e.g. £100 contribution + 25% = £125. £125 withdrawal – 25% = £93.75). With a Help to Buy ISA, you would miss out on the bonus, but no penalty would apply.

- If you want to use your LISA to save solely towards retirement, you could still use a Help to Buy ISA to save towards buying your first home. You can’t double-up and receive the Government bonus towards a house purchase from both accounts, though!

If you think that a Help to Buy ISA might be for you, you should get a move on! There are only 10 days remaining to open a new one. If you would like any further guidance, taking account of your individual circumstances, please get in touch and we will be happy to help.